What make listed company fall into PN17?

- MD

- Nov 7, 2022

- 3 min read

What is PN17?

PN17 stands for Practice Note 17/2005 and is issued by Bursa Malaysia; relating to companies that are in financial distress. Once the listed company falls into PN17, the company is at risk of being delisted from the Bursa Malaysia.

What are the criteria triggering PN17?

Listed company will falls into PN17 if triggered any one or more of the following:

1. Equity < 25% of Share Capital (excluding treasury shares).

Provision of Paragraph 2.1(a) The shareholders' equity of the listed issuer on a consolidated basis is 25% or less of the issued and paid-up capital (excluding treasury shares) of the listed issuer and such shareholders' equity is less than RM40 million.

2. At least 50% of the total assets taken control by receivers or managers.

Provision of Paragraph 2.1(b) Receivers or managers have been appointed over the asset of the listed issuer, its subsidiary or associated company which asset accounts for at least 50% of the total assets employed of the listed issuer on a consolidated basis.

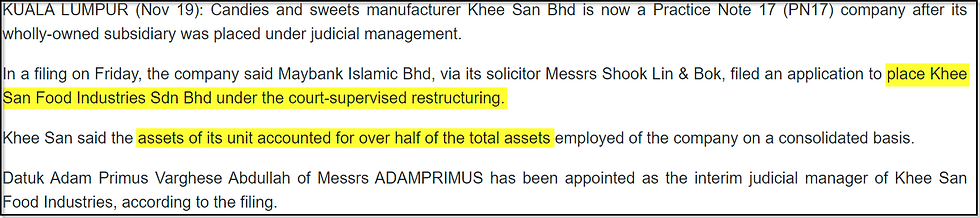

For example, in November 2021, Khee San Berhad triggered PN17 Paragraph 2.1(b) as its wholly-owned subsidiary Khee San Food Industries Sdn. Bhd placed under judicial management, and the assets of Khee San Food Industries Sdn. Bhd accounted for over 50% of the total asset of Khee San Berhad.

and in earlier month July 2021, there is news regrading to Khee San received demand letters from OCBC Al-Amin Bank.

3. At least 50% of the total asset are made up by winding up subsidiary/associated company.

Provision of Paragraph 2.1(c) Receivers or managers A winding up of a listed issuer's subsidiary or associated company which accounts for at least 50% of the total assets employed of the listed issuer on a consolidated basis.

For example, 04 Apr 2018, BERTAM ALLIANCE BERHAD triggered PN17 Paragraph 2.1(c) as winding up its wholly-owned subsidiary (Bertam Development Sdn Bhd). The assets of Bertam Development Sdn Bhd accounted for >50% of the total assets of BERTAM ALLIANCE BERHAD.

From the day earlier 02 Apr 2018, there is announcement regarding to the winding of Bertam Development Sdn Bhd.

4. Auditors expressed an adverse or disclaimer opinion on the company's financial statement.

Provision of Paragraph 2.1(d) The auditors have expressed an adverse or disclaimer opinion in the listed issuer's latest audited financial statements.

For example, SCABLE's external auditor said they not been able to receive sufficient appropriate audit evidence..

5. Auditors expressed concern on the company's ability to continue, and Equity< 50% of Share capital (excluding treasury shares).

Provision of Paragraph 2.1(e) The auditors have expressed an emphasis of matter on the listed issuer's ability to continue as a going concern in the listed issuer's latest audited financial statements and the shareholders' equity of the listed issuer on a consolidated basis is 50% or less of the issued and paid-up capital (excluding treasury shares) of the listed issuer.

For example, KNM's auditor uncertainty over its ability to continue..

& the company shareholders equity < 50% of share capital.

6. The (company/major subsidiary/major associated company) fails to pay a debt and is unable to declare about their ability to pay back the debts.

Provision of Paragraph 2.1(f) A default in payment by a listed issuer, its major subsidiary or major associated company, as the case may be, as announced by a listed issuer pursuant to paragraph 9.19A of the Listing Requirements and the listed issuer is unable to provide a solvency declaration to the Exchange.

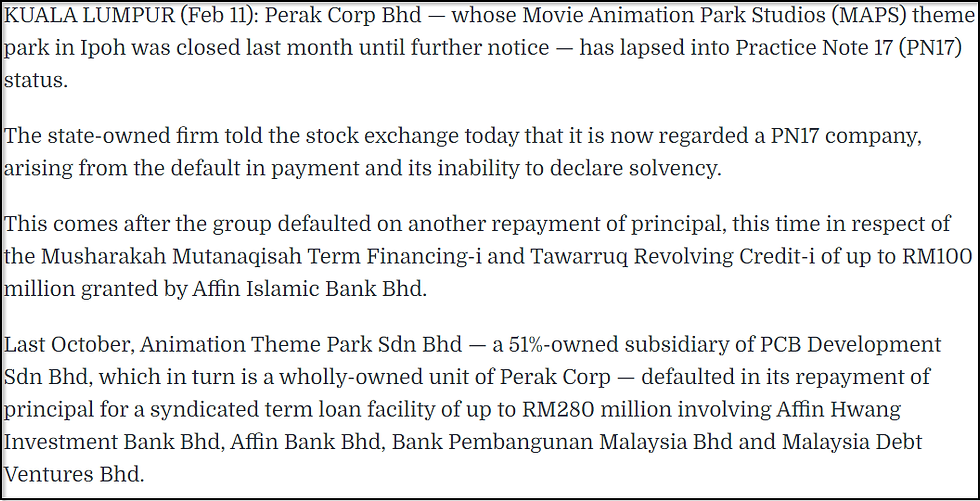

For example, PRKCORP falls into PN17 on 11 February 2020 as triggered PN17 Paragraph 2.1(f).

And before that, in October 2019, there was a news about PRKCORP unit defaults on loan payment.

Keep track with the company's news, announcements, and check on its financial statement.

Follow our facebook page for more information.

Comments